The dynamic landscape of the Canadian cannabis industry has been nothing short of transformative these past five years. Upon legalization, several LPs emerged as key market players, however, the recent shuttering of many cultivation facilities belongs to industry giants. Meanwhile, midsize LPs have displayed remarkable adaptability, navigating the challenges of running a cannabis business with limited capital and, in many cases, finding success.

Supply and demand shifts

The initial rush in the early days of cannabis legalization saw a proliferation of massive cultivation operations, often coupled with efforts to bring processing, extraction, packaging, and other activities in-house. The goal was clear: meet the projected demand of a budding industry. However, the reality was these grand-scale operations proved to be highly inefficient.

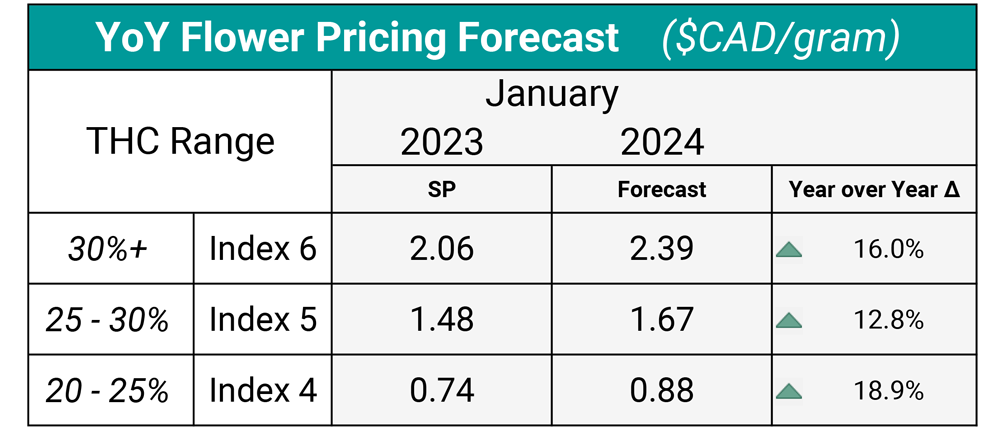

The oversupply issue hit its peak in late 2022 at the Canadian Cannabis Exchange (CCX), with wholesale prices reaching an all-time low of $0.74/gram in Q4 2022. The plunge in prices partially stemmed from the oversupply issue and from smaller LPs not having a path to access provincial retail markets. LPs big and small found themselves grappling with the repercussions of rapid expansion, vaults full of inventory, and managing over-built facilities. Awash with products, the natural consequence was a struggle to maintain pricing above breakeven. Now the tides are turning.

Over the past few years, reports have shown a 32 percent decrease in indoor and greenhouse cultivation from 2.2 million to 1.5 million square meters. Some large industry players such as Sundial, Canopy, and Aurora, had to make the painful decision to close large cultivation facilities. Similarly, several smaller LPs have also had to shutter operations or scale back cultivation rooms. These closures have disrupted established supply chains and resulted in shortages across several product categories. With this, we have seen buyers willing to pay higher prices to secure quality products. Transactions near and above $3.00 per gram wholesale are creeping back into the market for new harvests of high THC (30%+), craft-grown products.

Emerging midsize LPs

Amid the over-supply turmoil, midsize LPs, often nimble and more flexible in their approach, found a way to adapt. The challenge of running a business with limited capital led them to focus on efficiency, innovation, and specialization. Their ability to pivot became a driving force in the industry’s transformation. We’ve observed a market shift toward right-sizing the cultivation footprint and activities offered to meet market demands, focusing on core competencies and building effective teams.

Regulatory challenges and pricing dilemmas

Nevertheless, challenges persist and many of them revolve around regulation. Taxation, licensing fees, limits on marketing activities, and the burden of reporting activities are among the hurdles LPs face.

Many of them will need to change to increase industry viability, but the most direct factor on wholesale pricing down pressure stems from the provincial buyers.

Provinces have been hesitant to raise cannabis prices, influenced by their need to compete with the illicit market on top of the public’s insistence on lower prices driven by a 4.8 percent inflation increase.

Wholesale buyers are also constrained in their ability to raise their purchase price for products due to the fixed SKU prices set at the provincial level. Multiple buyers are now vying for the same use cases at similar wholesale pricing levels. Those buyers willing to increase wholesale purchase prices often find themselves unsustainably compromising their margins to fulfill purchase orders, and unless provincial prices increase, the market will continue to face a ceiling on pricing and depressed margins. CCX has however witnessed substantial growth in international trades, with an average transaction price of $4.10/gram.

As we approach 2024, critical questions will shape the upcoming year in cannabis: Will provinces and consumers accept higher prices for cannabis products? Will we continue to see facility shutdowns without a clear path to profitability? Will the CRA enforce the collection of back taxes from LPs? Will the legislative review of the Cannabis Act bring meaningful reform? The answers to these questions will determine the direction of the Canadian cannabis industry, shaping its challenges and opportunities in the years to come.